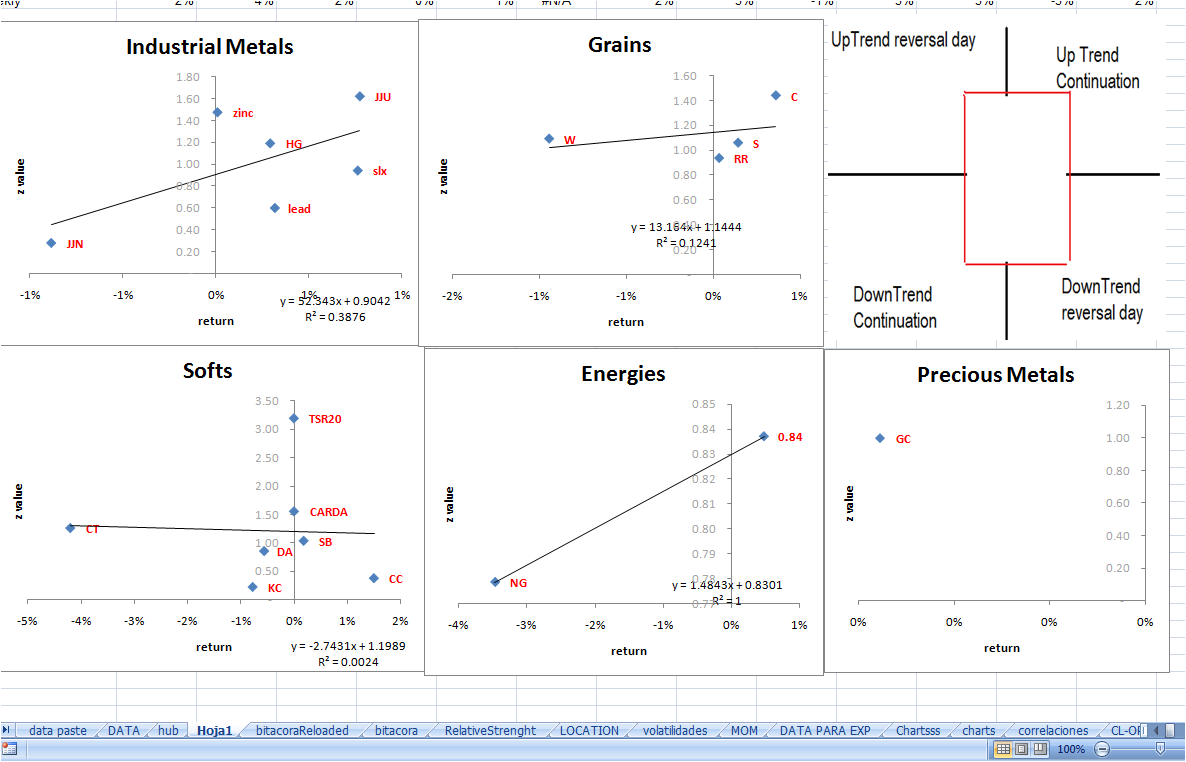

this print screen will serve me as a reference in the future regarding the steepness of the market and the day’s percentage return for the 2010 start.

The steepness of the mkt is measured by the z value of the last 67 days, meaning:

For the last 67 sessions please compare the average return with the normal volatility for a single day: average divided the result of dividing standard deviation in the square root of 67. If the result is grater than three, then the avg return is consistent because the normal growth is three times the usual volatility.

If I compare the 67-day resume against today’s return, then we can infer if we are in continuation, reversal or neutral activity according to the prevailing trend; like a strike zone as the one the upper right side red square.

I think this is a good method for discriminating what markets should be excluded from sight or maybe a pattern-report for building more abstract positions like selling volatility (inside the red strike zone) or getting other trend following positions for the ones outside the red square.

Back Testing it is the next step.