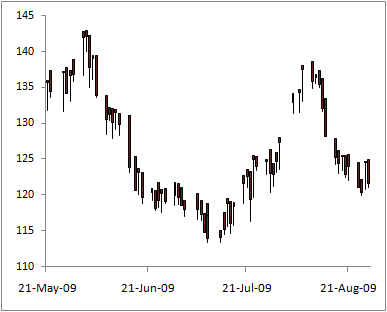

When I began to write this post I was about to say that coffee is more volatile from the rest of the markets I follow. But then I thought “before thinking about this, I should rank the relative ATR for this mkts”. Here is what we have:

Coffee is not the most volatile commodity among my tickers. Basically those are energies like NG and CL… and sugar. NG is almost double KC’s average true range related to the last closing price.

There is a little opportunity here: We have upward potential for 5 and twenty two days with a z value of two and 47% and 35% probability of loss respectively. But the expected value are too short: 1% for the 5 day strategy and 4% for the 22day. This is not based on ATR but in an indicator, which I was learned a couple of semesters ago, named Location which basically measures how away is the last price from its trends resumed by long term moving averages.

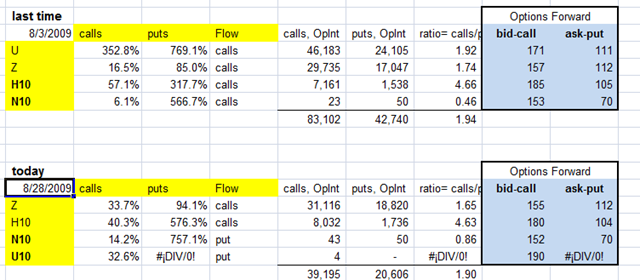

Also I want to see the Options. And we have this:

One month ago from this post the call/put ratio was 1.94 and today it is 1.90. No difference you may say. But the open interest dropped 53%. There was 83k calls in the beginning of august and 42k puts.

So in options we have the same “expected” scenario but with lesser voters willing to risk their capital supporting this.

Apparently in KC the bid call indicador [email me if want to know about this at joachin[at]ufm.edu] the singal is a reversal because we have had call weight but puts’ levels are closer to reality.

What if we sell some calls at 160 and sell some puts at 112 in the Z month? Let us paper trade it.