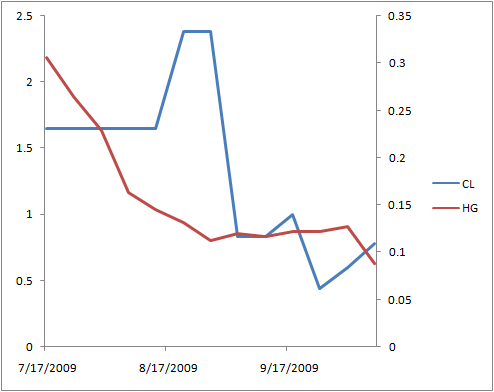

67 day correlation between CL and HG is 0.60. 1400 day correlation is 0.37. This is saying that both commodities have been extremely friendly each other and that is not regular.

This is a paper trade of 90 days, so I will chose January options:

I will be willing to risk two thousand dollars and would be satisfied with with a R of 3, so a profit of six would be a like double play in a tied game.

B 1 CLF10-9500C @ 1.08

B 1 HGF10-240P @ 0.08

Debit account if margin would equal 100% = -1.08*1000 -25000*0.08 = -$3080 minus fees and commissions.

I should notice that I am seeing CL and HG but actually I would be trading derivatives on these futures; i.e. options prices might not be correlated and risk is being amplified.

The fact that both positions will be long options doesn’t mean risk of loss is being reduced because of greek fundamentals. I mean, The max loss would be 100% of the position, but the probability of hitting -100% is higher, so the trade is actually quite maverick-like. Using futures volatility is high, but liquidity risk is lower.

According to my position, both red and blue line will go up. Maybe it would better using spreads instead of naked long options.

THIS POSITION WILL BE CLOSED ON FRIDAY DECEMBER 18 2009.

One comment