Probably my experience in baseball is as documented as in trading. Very low for an average standard. I am not in the major league in my country [which is very bad in a word standard] neither I am a full time trader taking and handling positions with my own money. In baseball I just pitch for a 3rd level league (Mantarrayas is the name) and in trading I am just a commodity markets risk analyst. I suppose to manage hedging positions of clients but that is another story. Even though I do manage positions, not of my speculative mine, but the hedging account of my boss who is a 10-year-experienced trader. For example now I am looking 2 options-spread trades one in the SP500 mini and other in the euro futures. Also a paper trade of mine which I just posted last time I decided to write here.

Well enough BS. I planned to talk about the relationship between the strike/ball account and the performance of a system or a trader.

As a pitcher the best thing you can have is either a strikeout [3 strikes] or a hit managed by your defense like a ground ball or a fly ball.

Pitching is hard because first of all you have to be able to put the ball in the strike zone at a decent velocity. The pitchers you see in the TV are the exception of the rule because most of the time they are able to make more strikes than balls. Most of humans that like baseball cannot locate a decent fastball more than 2 or three times around the strike zone. Much less people can play with the catcher hitting the corners and moving the ball with plain vanilla curve balls or only variation of a fastball. Pitching is hard and most of the times homo-sapiens don’t realize until we try it.

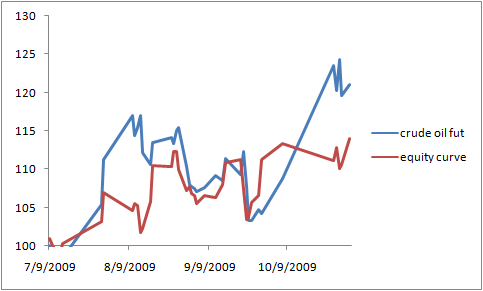

As I extend in my lunch time while I see the TY, SP and CL, I try to make a point, I am just getting stuck with baseball.

Ok. Few days back a I saw a mlb playoff game and one of the pitchers had 101 pitches 69 of them strike. That’s a strike ratio of 2.15, meaning 2 strikes for one ball. He was able to get ahead of the hitter most of the time. If you consider a win/lose ratio of a trading system, for example one I am testing now: it is a -0.6% avg lose and +0.2% winner, or a strike/ball ratio of 0.39. That like a 101 pitches with 29 strikes, a very very poor performance.

I have made about 14 trades in the corn futures. two of them were profitable. And losses were extremely heavy. I have opened about 4 games in my baseball career since 2008, and only one of them were mediocre, the rest were very bad. I don’t have the strike/pitch count.

What system or approach should I use to improve in these both environments that I like so much? I even gained weight and every day I am very poor making it impossible to even put some dollars for a little spread trade in the oil market. Is this really for me? Was I designed for baseball and trading? What strategies must me thought to accelerate the truth of these questions?