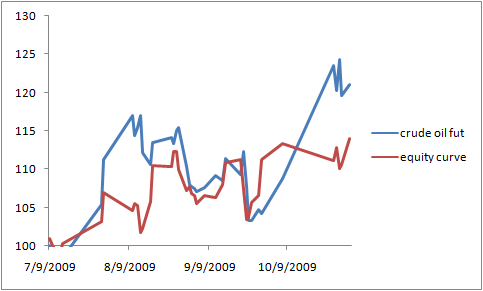

testing oil intra day with the Vwap

Signal of the coach: go long at 830am if yesterday you had a positive VWAP. If not, do nothing.

from July 3rd to November 5th.

Result: It would have been better parking the money on a long position get it out today. The market return was higher and we are not considering transaction and slippage costs.

You might say: try leverage!

Well I am not sure with this facts:

z value: 1.05

w/L ratio: 1.29

So what I will do is run the whole process back testing the adverse intra day scenarios. Leverage to use will be 1:3 since the max loss is -3.7% then that would be 12% draw.

Any way the short z value tells me that with leverage I just will turn figures up. Unless I systematize the leverage: check if the strategy has a pattern to increase positions because of a given opportunity.

Also using only price, and a good z-value means some supply/demand effect converted intro profits.